SOCIAL SECURITY & MEDICARE PROTECTION

Make America Grow Again: Episodse 18 | How Wall Street Privatization and Pharma Pricing Are Targeting Social Security and Medicare

STOP SCROLLING: The Retirement Crisis Isn’t Real. The Heist Is.

Timeline: 12–18 months for immediate fixes

Core Targets: Wall Street privatization schemes + pharmaceutical price manipulation

The First Truth Most Politicians Won’t Say

You’ve paid into Social Security your entire working life.

Roughly 12.4% of every paycheck disappears before you even see it. Not optional. Not voluntary. Mandatory.

In 2024, the average American contributed $10,453 toward Social Security and Medicare.

So here’s the uncomfortable question:

Why are politicians warning the system is “going broke” while Wall Street firms are pitching plans to manage your retirement money for a fee?

Because this isn’t a fiscal emergency.

It’s a manufactured crisis.

Welcome to the retirement robbery: a decades-long campaign to convince Americans that the most successful anti-poverty program in U.S. history is failing, just in time for private finance to step in and profit.

The Numbers They Hope You Never Look Up

Before opinions, facts.

16.5 million seniors lifted above the poverty line by Social Security (2024)

Poverty among Americans 65+ would be 38.7% without Social Security

→ Today: 9.2%Trust fund solvent until 2034

After 2034: 77% of benefits payable indefinitely even with zero reforms

Removing the payroll tax cap extends solvency beyond 2060

Medicare covers 65 million Americans

Expanding Medicare could save $450 billion annually

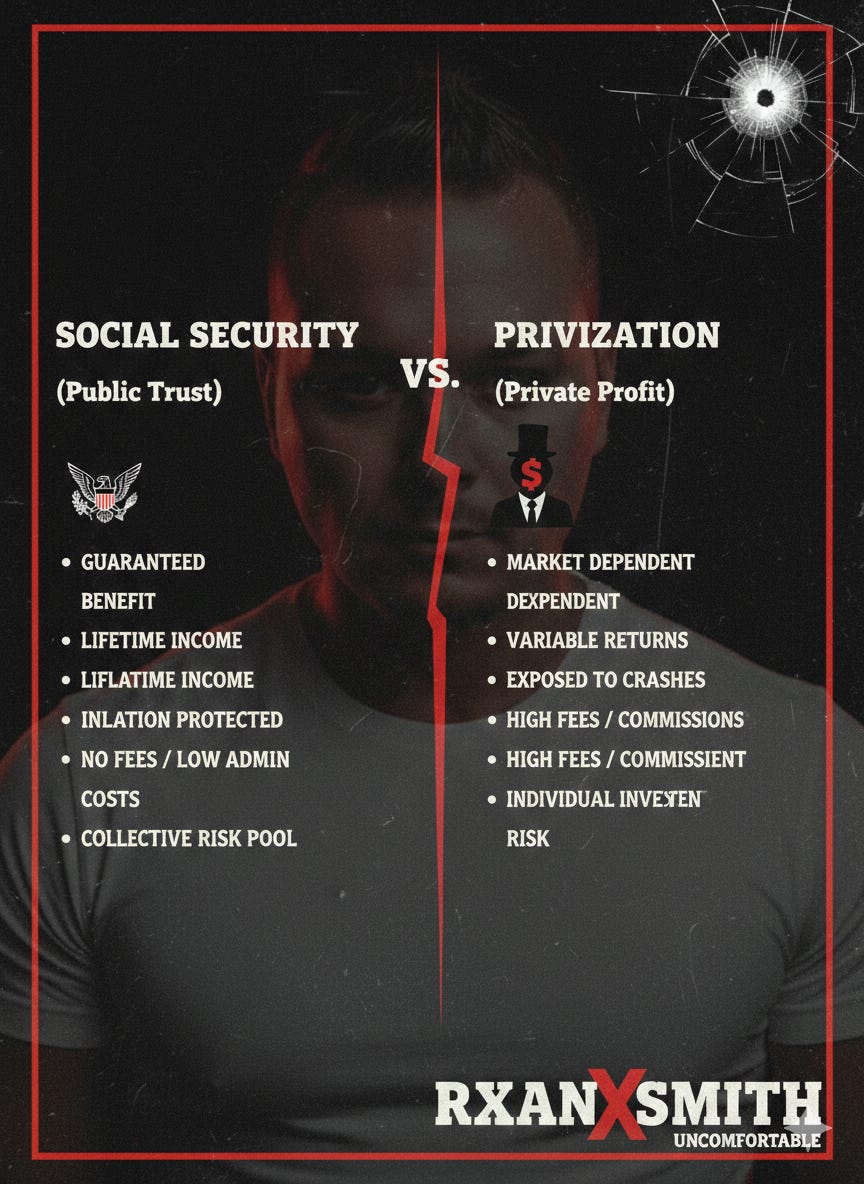

Social Security admin costs: 0.6%

Wall Street retirement accounts: 1–2% annual fees

Translation: the system isn’t collapsing.

Someone just wants access to it.

THE MANUFACTURED CRISIS

It’s Not Broke. It’s Targeted.

The Core Thesis

Social Security and Medicare are not failing programs.

They are politically weakened on purpose.

For over 40 years, a coordinated narrative has repeated one message:

“Government retirement programs are unsustainable.”

Not coincidentally, that message appears whenever private financial firms propose managing retirement funds themselves.

The Math Politicians Skip

Social Security pays 100% of promised benefits through 2034

After that, it still pays 77% indefinitely

Compare that with private markets:

The 2008 financial crash erased $2.8 trillion in retirement savings

Social Security payments never missed a check

Guaranteed benefits did exactly what insurance systems are supposed to do: remain boringly reliable.

What Makes the “Crisis” Unique

Social Security is judged using 75-year projections.

Name another federal program held to that standard.

The military budget isn’t. Tax cuts aren’t. Corporate subsidies aren’t.

Only the program ordinary Americans rely on most.

THE PRIVATIZATION SCAM

Wall Street’s Real Retirement Plan

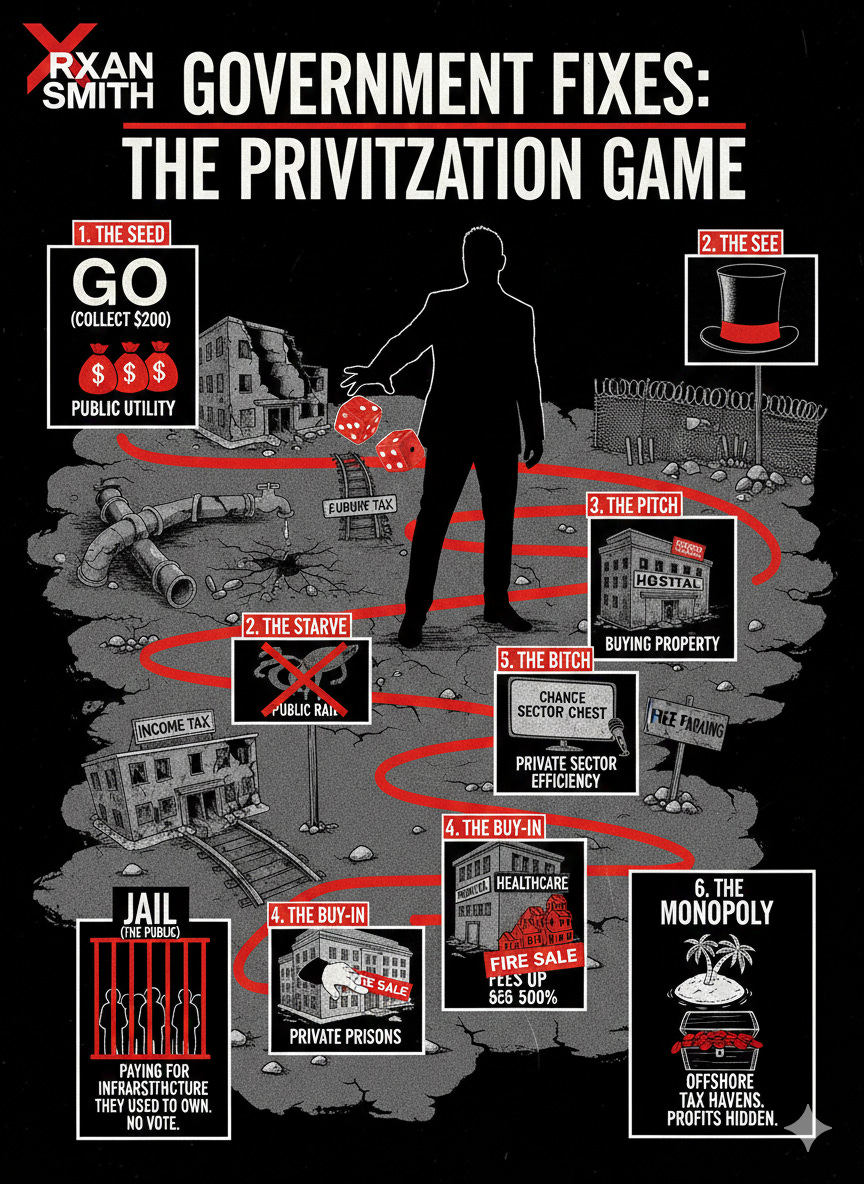

The Timeline of the Heist

1980s: Privatization ideas emerge during Reagan-era reforms

2005: George W. Bush proposes private accounts (public backlash kills plan)

2010s–Present: Rebranded as “entitlement reform”

2024+: Private equity openly lobbying to manage Social Security funds

Same idea. New marketing language.

T

he Fee Extraction Machine

System Administrative Cost Social Security 0.6% Private Accounts 1–2% annually + trading fees

On a $500,000 retirement account over 30 years:

Social Security admin costs: ≈ $90,000

Wall Street fees: $450,000–$900,000

That isn’t reform.

That’s revenue extraction.

Case Study: Chile’s Privatization Experiment

Privatization promised freedom and higher returns.

Reality:

Half of retirees received below minimum pensions

Replacement rate fell from 70% → 34%

Mass protests forced partial renationalization in 2019

Risk moved to retirees. Profit stayed with financial firms.

The 2008 Stress Test

If privatization had passed in 2005:

Retirement benefits could have dropped 40–50% overnight

Millions of seniors pushed into poverty

Instead, Social Security paid every benefit in full.

Predictability beat speculation.

MEDICARE: THE PROGRAM PHARMA CAN’T CONTROL (YET)

What Medicare Actually Does

Covers 65 million Americans

Admin costs: ~2%

Private insurance admin costs: 12–18%

Satisfaction rate: 88%

Without Medicare, average senior insurance costs exceed $7,500 annually.

Why It’s Under Attack

Medicare represents something dangerous to corporate healthcare:

proof that public insurance can be cheaper and more efficient.

The Medicare Part D Catch

In 2003, Congress created prescription drug coverage.

Hidden clause:

Medicare was legally banned from negotiating drug prices.

Result:

Insulin ≈ $300/month in the U.S.

≈ $30/month in Canada

Pharmaceutical lobbying spending: $116 million.

Policy outcome: guaranteed pricing power.

Not market competition. Legislated leverage.

ITHE GENERATIONAL WAR MYTH

You’ve heard this one:

“Social Security is stealing from young people.”

Convenient narrative. Completely misleading.

Reality

Social Security is insurance, not an investment account

Every generation contributes

Every generation receives benefits

Workers earn future eligibility through contributions

The real intergenerational transfer isn’t retirees.

It’s policy choices.

The Actual Wealth Drain

Tax cuts for the wealthy: $2 trillion

Corporate subsidies: $1 trillion annually

Military spending: ≈ $900 billion/year

Student debt burden: $1.7 trillion

Thos aren’t demographic inevitabilities.

They’re decisions.

THE FIX: PRACTICAL REFORMS (12–18 MONTH WINDOW)

Immediate Actions (Year 1)

✅ Lift the Payroll Tax Cap

Current cap: $168,600

Proposal: raise to $400K or remove entirely

Effect: solvency beyond 2060

Impacts top ~6% of earners

✅ Allow Medicare Drug Negotiation

Repeal 2003 negotiation ban

Estimated savings: $450 billion / decade

Lower premiums, extended solvency

✅ Tax High Investment Income for Social Security

Apply payroll tax to investment income above $400K

Adds ≈ $100B annually

Medium-Term (Years 2–5)

Increase benefits for low-income seniors

Expand Medicare coverage

Automatic funding adjustments tied to demographics

Long-Term Protections (5+ Years)

Constitutional protection for Social Security

Public banking alternative to private retirement extraction

MYTHS VS. REALITY

Myth: Social Security is going broke

Reality: Fully funded to 2034, mostly funded forever.

Myth: Young people won’t get benefits

Reality: Only true if benefits are cut instead of revenue adjusted.

Myth: Private accounts perform better

Reality: Markets crash. Guaranteed benefits don’t.

Final Thought

Social Security and Medicare aren’t collapsing. They’re being marketed as collapsing. And there’s a difference. When politicians say these programs are “unsustainable,” what they often mean is they’re unsustainable for people who don’t already make money off them. Think about it: Social Security has paid every benefit through wars, recessions, and financial crashes. Wall Street needed a bailout in 2008. Social Security didn’t. Yet somehow the stable system is called the risk, and the risky system is called the solution.

This debate isn’t really about math. The math mostly works. It’s about control. Who controls the largest guaranteed pool of money in America? A public system designed to prevent elderly poverty, or private firms that see retirement as just another revenue stream?

Because once stability becomes a product, security turns into a subscription plan. And the real question isn’t whether these programs survive. It’s whether retirement remains a promise we make to each other… or just another bill you have to keep paying until the day you die..

Take Action: This Needs Your Voice

If

If you’re done with the performance art of caring about rural America or left vs. right wars in general, while watching it burn support my work, consider becoming a free or paid subscriber. It takes a village. I only have a pen.

Share this article - Send it to someone who still thinks “market forces” are natural

What’s the biggest scam you’ve seen in rural decline?

PayPal Pledge Support - Independent media survives because readers fund it.

I don’t run ads. I don’t take corporate money. I don’t soften the truth to keep sponsors happy. That means I need you.

One-time support:

$5 | $10 | $20 | $50 | $100

Monthly support:

Subscribe - $5/month | Founding Member - $50/month

Every dollar goes toward research, writing, and exposing the systems that profit from your suffering.

Connect With Rxan Smith Across the Web

📺 YouTube🐦 X (Twitter)📸 Instagram (Main)📸 Instagram (Alt)🧵 Threads (Main)🧵 Threads (Alt)📘 Facebook☕ Buy Me a Coffee💰 PayPal🎭 Patreon

25 Fixes Make America Grow Again (Full List)

rxansmith.substack.com · YouTube: @RealRxanSmith · X: @rxannsmith

— Rxan Smith

Uncomfortable

Making America Grow Again, One Uncomfortable Truth at a Time

Reading this felt a bit like having someone switch on a harsh fluorescent light in a room we preferred in shadows, and yet it is needed. I appreciated how you connected the policy details to the very human fear of aging into precarity. It made me see how “systems” are really just stories we write about who deserves to feel safe when they are most vulnerable.

Rxan, Thankyou for breaking this down so a child can understand 🫶💖